Charting Intersections Between Digital Currency Incentives and App-Based Reward Pathways

Digital currency incentives have expanded rapidly across mobile platforms since the early 2020s, creating measurable overlaps with traditional app-based reward systems that track user engagement through points, tiers, and redemptions. Researchers tracking these developments note that blockchain ledgers now underpin loyalty mechanisms in finance, retail, and service applications, allowing tokens or stablecoins to replace or supplement conventional points while maintaining verifiable transaction histories.

Core Components of Digital Currency Incentives

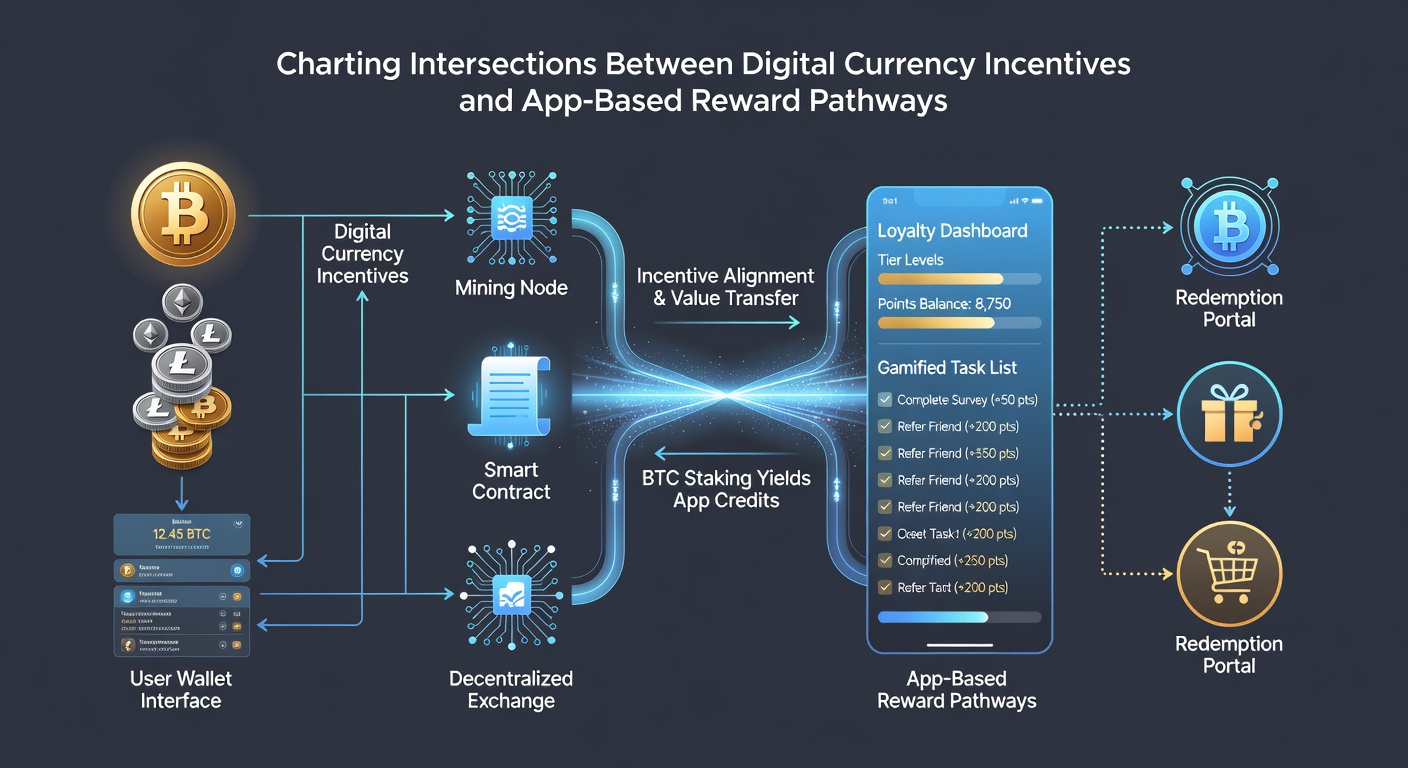

Digital currency incentives typically operate through programmable tokens distributed via smart contracts, and data from multiple industry analyses shows these mechanisms reward actions such as transaction volume, referral completions, or sustained platform activity. Stablecoins pegged to fiat currencies appear frequently in these structures because they reduce volatility compared with unpegged cryptocurrencies, enabling users to accumulate value that can later convert into goods, services, or further digital holdings without intermediate exchange steps. Observers note that integration often occurs through API connections between wallet providers and app backends, which streamlines the transfer of incentives directly into user accounts.

Mechanics of App-Based Reward Pathways

App-based reward pathways rely on centralized databases that log user behaviors and calculate eligibility for benefits according to predefined algorithms. These systems frequently employ tiered structures where accumulated activity unlocks escalating rewards, and studies from academic institutions have documented how such pathways encourage repeat engagement across sectors. When platforms incorporate digital currencies, the underlying ledger replaces portions of the centralized database, providing immutable records of point issuance and redemption while still preserving familiar user interfaces for participants who may not interact directly with blockchain elements.

Points of Intersection in Practice

Intersections emerge when apps permit users to exchange earned points for digital currency holdings or vice versa, creating hybrid economies within single platforms. In June 2026 several major retail and financial applications reported expanded functionality allowing seamless conversion between loyalty points and selected stablecoins, a development tracked through public disclosures and developer documentation. These conversions rely on predefined exchange rates maintained by the app operator, and researchers have observed that transaction fees remain lower than those associated with external cryptocurrency exchanges because settlements occur within the controlled environment of the app ecosystem.

Another intersection appears in referral programs where both referrer and referred users receive digital currency credits upon successful onboarding, and these credits then feed into the broader reward pathway as spendable balances. According to a Bank for International Settlements analysis, such dual-currency systems reduce friction for users already familiar with app rewards while introducing them to digital asset concepts without requiring separate wallet management. Data indicates that platforms adopting this model often experience higher retention rates during the first ninety days of user activity compared with purely points-based predecessors.

Regulatory and Technical Considerations

Regulatory frameworks in multiple jurisdictions now address how digital currency rewards intersect with consumer protection rules originally designed for traditional loyalty programs. The Australian Securities and Investments Commission and the Monetary Authority of Singapore have issued guidance requiring clear disclosure of conversion terms and associated risks, while Canadian provincial regulators have examined tax implications when rewards transition into taxable digital assets. Technical standards developed by industry consortia emphasize interoperability between legacy reward databases and distributed ledgers, ensuring that audit trails remain intact even when value moves across different asset classes.

Security protocols at these intersections combine established app authentication methods with cryptographic key management, and organizations such as the World Economic Forum have published reports detailing best practices for safeguarding user holdings during conversion events. Implementation varies by region because local data residency requirements influence where ledger nodes and user data repositories are physically located.

Emerging Patterns Across Sectors

Finance applications lead adoption by linking credit card rewards directly to stablecoin deposits that users can later deploy within decentralized finance protocols, whereas retail apps more commonly use digital currency incentives for supplier payments or customer cashback programs. Service sector platforms, including ride-sharing and delivery services, have tested models where drivers accumulate cryptocurrency credits that automatically convert into local currency at the end of each shift, reducing volatility exposure for participants. These varied implementations demonstrate that the intersection between digital currency incentives and app-based reward pathways adapts to sector-specific needs while preserving core principles of verifiable issuance and user-controlled redemption.

Conclusion

The mapping of intersections between digital currency incentives and app-based reward pathways continues to evolve through incremental technical integrations and regulatory clarifications. Evidence from regulatory filings, academic studies, and platform disclosures indicates sustained development across multiple regions as of mid-2026, with interoperability standards and consumer protection measures shaping how these systems function in daily use. Future documentation of these trends will likely focus on measurable outcomes in user retention, transaction volumes, and cross-border compatibility as the underlying technologies mature.